In the high-stakes world of digital banking, the pressure to deliver new features is relentless. Whether it’s a new regulatory requirement or a trending fintech integration, the demand for “fast” often leads to compromised architectural decisions. This creates what we call Technical Debt, a silent velocity killer that starts as a minor inconvenience and ends as a massive roadblock for innovation.

The True Cost of “Quick Fixes”

When a development team bypasses long-term scalability for a short-term release, they aren’t just saving time; they are borrowing it from the future. In banking systems, where security and data integrity are non-negotiable, this debt accrues interest rapidly. Eventually, the team spends more time managing regressions and “patching the patches” than building actual value. This is why a feature that took one week to deploy two years ago might take two months today.

Breaking the Dependency Trap

The primary symptom of unmanaged technical debt in banking is tight coupling. When core banking functions are intertwined with UI logic or third-party integrations, a single change in the interest rate calculation engine might unexpectedly break the mobile login flow. At Mavidev, we tackle this by enforcing a strict separation of concerns. By utilizing an Interface-First approach, we ensure that modules communicate through well-defined contracts rather than direct dependencies. This allows us to swap or upgrade internal logic without causing a ripple effect across the entire ecosystem.

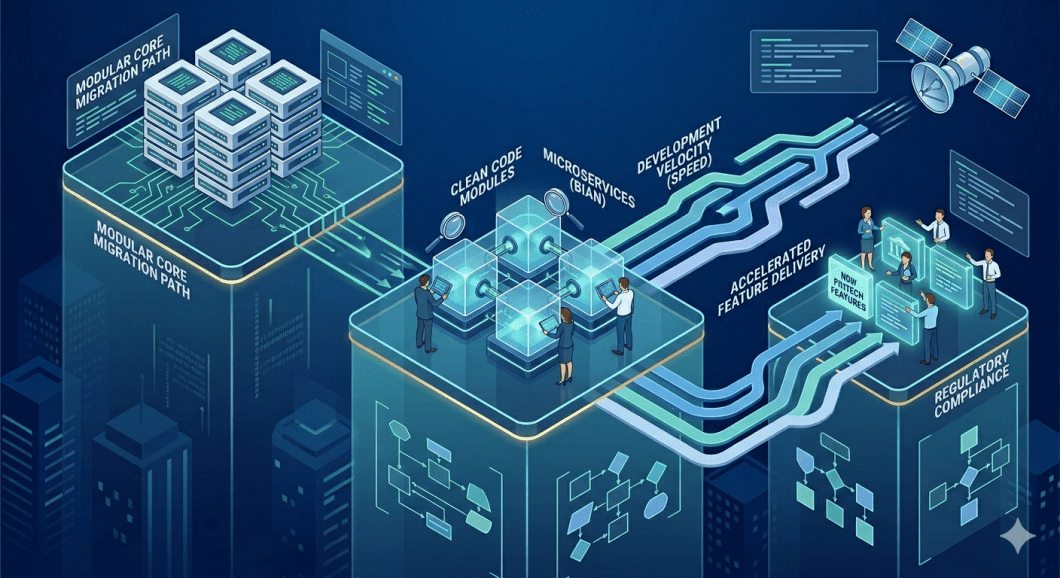

Modernizing Without the “Big Bang” Risk

One of the biggest misconceptions in the industry is that technical debt can only be solved by a total system rewrite. In reality, a “Big Bang” migration is often too risky for financial institutions. Instead, we advocate for the Strangler Fig Pattern. This strategy involves incrementally migrating functionality from legacy monoliths into modern, modular microservices. By building a protective “Anti-Corruption Layer” between the old and the new, we ensure that data remains consistent while the system evolves. This method allows the bank to maintain its operational pace while systematically “strangling” the technical debt out of existence.

From Observation to Resolution

Managing debt requires more than just good intentions; it requires visibility. Building on our previous discussion about Operational Observability, we use deep system insights to identify where the “friction” is highest. If our observability tools show that a specific service is consistently slow or prone to errors after every update, we know exactly where the technical debt has reached its limit. This data-driven approach turns refactoring from a “gut feeling” into a strategic investment.

Velocity as a Strategy

Technical debt is not a sign of failure; it is a natural byproduct of growth. However, leaving it unmanaged is a strategic risk. For a bank to remain competitive, its software must be as liquid as its assets. By prioritizing modularity, automated testing, and incremental modernization, we help our partners reclaim their development velocity and turn their technology stack back into an engine for growth.